Mobile banking app development has become one of the most security-critical areas of digital product engineering. Global mobile banking users passed 2.17 billion, and fraud has scaled right alongside that growth. For companies, that means resilient codebases, secure APIs, and continuous monitoring must be planned from the start. The financial impact of getting this wrong is significant. IBM’s report found that the average cost of a data breach in the financial sector was $6.08 million, making financial services one of the costliest industries for security incidents. In 2026, that pressure is even greater as attackers automate phishing, exploit weak APIs, and target mobile banking flows that connect directly to customer funds and sensitive personal data.

This guide walks through the threats banking apps face, the regulations that shape how you build, the architecture and process decisions that hold up under pressure, and what all of this costs in practice.

What is a mobile banking app?

A mobile banking app is a smartphone application that lets users access banking services (e.g., checking balances, transferring funds, paying bills, etc.) through a secure connection to the bank’s backend systems. It combines consumer-facing UX with financial-grade security, strict regulatory compliance, and robust, scalable infrastructure.

Types of mobile banking apps

- Retail banking apps serve individual consumers with everyday banking (accounts, payments, cards, loans, and basic savings).

- Digital-only banks (neobanks) are fully digital institutions with no branches; they rely heavily on mobile apps as their primary interface.

- Credit union apps are member-owned financial cooperatives that offer services similar to retail banks, often with a focus on community and lower fees.

- Corporate banking apps are designed for business customers, supporting multi-user access, approvals, bulk payments, and integration with accounting systems.

- Investment banking apps are tailored for asset management, real-time equity trading, fractional share execution, and secure data-heavy market analytics streams.

- Wallet/payment apps focus heavily on near-field communication (NFC) protocols, point-of-sale terminal interactions, and quick QR-code payment generation.

How banking apps differ from other financial apps

Most financial apps primarily visualize information or facilitate limited financial activities. Banking apps, by contrast, directly access customer deposits, initiate regulated financial transactions, and connect to core banking infrastructure in real time. A successful attack can result in immediate financial loss rather than simply exposing user data. This creates much higher expectations around security, compliance, and operational resilience.

In other words, while many financial apps focus primarily on delivering convenient digital experiences, mobile banking apps must simultaneously protect customer funds, preserve trust, satisfy regulators, and remain available around the clock.

Must-have features mobile banking apps should include

Customer expectations for mobile banking have changed dramatically over the past decade. The challenge for companies isn’t to build every possible feature at once but to prioritize capabilities that deliver the greatest value while maintaining security, compliance, and performance.

Features to give users from day one

1. Account dashboard. The dashboard is the heart of every banking app. Users should be able to instantly view account balances, pending transactions, recent activity, and available funds without unnecessary navigation. Information should refresh in near real time while clearly distinguishing between pending and completed transactions to avoid confusion.

2. Fund transfers. Customers expect to move money quickly and securely. A modern banking app should support:

- Transfers between a user’s own accounts

- External bank transfers

- Peer-to-peer (P2P) payments

- Scheduled and recurring transfers

- Transfer history and confirmation receipts

High-risk transfers should trigger additional authentication based on contextual risk rather than applying the same verification to every transaction.

3. Bill payments. Integrated bill payment functionality allows customers to manage utilities, subscriptions, credit cards, mortgages, and other recurring expenses from a single interface. Features like automatic payments, reminders, and payment history improve convenience while reducing missed payments.

4. Push notifications. Real-time notifications improve both customer experience and fraud detection. Common notification types include:

- Successful transactions

- Failed payment attempts

- Large withdrawals

- Login from a new device

- Password or profile changes

- Card usage alerts

- Low balance warnings

5. Card management. Customers expect to manage payment cards without contacting customer support. Self-service controls typically include:

- Freeze or unfreeze cards instantly

- Report lost or stolen cards

- Adjust spending limits

- Enable or disable international transactions

- Control online or contactless payments

- View digital card details for online purchases

6. Biometric authentication. Biometric authentication has become a standard login method across both iOS and Android devices. Fingerprint recognition, Face ID, facial recognition, or device biometrics allow users to authenticate quickly while reducing reliance on passwords.

For higher-risk activities, biometrics should be combined with contextual authentication or additional verification factors rather than used as the sole security mechanism.

7. Customer support access. When financial issues arise, users expect immediate assistance without leaving the app. Modern banking applications commonly integrate:

- Live chat

- AI-assisted customer support

- Secure messaging

- Callback requests

- Fraud reporting

- Branch and ATM locators

8. Statement downloads and digital documents. Users should be able to access account statements, tax documents, loan agreements, and other banking records directly from their mobile devices. Secure PDF generation, searchable archives, and encrypted document delivery improve convenience while supporting regulatory recordkeeping requirements.

Features that will keep you competitive

1. Real-time spending categorization and budget tracking. Automatically categorizing transactions helps customers understand their spending habits without having to manually review every purchase. Spending dashboards, monthly summaries, and personalized budgets encourage greater financial awareness and increase engagement with the app.

2. Payment notifications with merchant information. Modern banking apps enrich payment notifications with merchant names, logos, locations, maps, and purchase categories. These contextual details make transactions easier to recognize while helping users identify unauthorized activity more quickly.

3. In-app loan applications. Customers increasingly expect to apply for personal loans, mortgages, or credit products without visiting a branch. By integrating identity verification, credit assessment, and automated underwriting, banks can provide near-instant eligibility decisions while simplifying the lending process.

4. Investment and savings products. Many financial institutions now offer investment accounts, high-yield savings products, retirement planning, and automated savings tools in a single application. Keeping these services inside a unified platform reduces friction and encourages customers to consolidate their financial activities.

5. Mobile check deposit. Although digital payments continue to grow, mobile check capture remains an important capability in many markets. Customers can deposit checks by photographing both sides, while backend systems validate image quality, detect duplicate submissions, and perform fraud checks before processing the deposits.

6. Multi-currency accounts and global transfers. For customers who travel frequently or conduct business internationally, support for multiple currencies and cross-border payments is invaluable. Features often include:

- Multi-currency balances

- Real-time exchange rates

- International payment tracking

- Transparent fee calculations

- Local payment network integrations

7. AI-powered financial insights. AI enables banks to move beyond static account information by providing personalized recommendations such as:

- Spending trend analysis

- Subscription detection

- Savings opportunities

- Cash flow forecasting

- Budget recommendations

- Personalized financial health scores

8. Open banking integrations. Open banking allows customers to securely connect accounts from multiple financial institutions into a single interface. This provides a more comprehensive financial picture while enabling budgeting, lending, and wealth management services built on aggregated financial data. Because Open Banking relies heavily on APIs and third-party integrations, robust authorization controls and continuous monitoring are essential.

Features that are getting momentum in 2026

1. Conversational AI for banking assistance. AI assistants provide contextual support for tasks such as explaining transactions, answering policy questions, guiding customers through financial processes, and helping resolve common issues. The most effective implementations keep humans in the loop for complex requests while using AI to reduce response times and improve service availability.

2. Embedded investment products. Banks are integrating investment services directly into their mobile apps, allowing customers to purchase fractional shares, automate recurring investments, and diversify portfolios without switching platforms.

3. Real-time fraud alerts. Rather than simply notifying customers of suspicious activity, newer banking apps enable users to verify or dispute transactions directly from the notification. This shortens fraud response times and helps institutions limit financial losses.

4. Crypto wallet integration. While regulatory approaches vary across jurisdictions, some financial institutions are beginning to integrate regulated digital asset services into existing banking applications. These may include cryptocurrency custody, trading, or wallet functionality supported by appropriate compliance controls.

5. Carbon footprint tracking. Some banks now estimate the environmental impact of customer purchases based on transaction data. By providing carbon footprint insights and sustainability recommendations, financial institutions can support customers interested in making more environmentally conscious spending decisions.

Why security is the foundation of mobile banking apps

Security decisions shape customer trust, financial losses, regulatory standing, brand reputation, and the bottom line all at once. Here’s how:

| Customer trust | Regulatory compliance | Brand reputation | Financial losses |

|---|---|---|---|

| Users won’t adopt or keep an app they don’t trust. A single breach can destroy confidence for years. | Regulators expect documented, tested security controls and evidence that they work. | Public incidents lead to negative media, loss of partners, and regulatory scrutiny. | Beyond direct fraud losses, breaches trigger fines, legal costs, and operational disruption. |

Banking apps connect directly to real money and sensitive personal data, which makes them a consistently attractive target: attackers can monetize a compromised account within minutes. The scale backs this up. The Anti-Phishing Working Group recorded 989,123 phishing attacks in a single quarter. Microsoft reports that password-based attacks account for more than 99% of the roughly 600 million daily identity attacks it tracks, and that its systems block around 7,000 password attacks per second. When a breach occurs, the damage extends well beyond the immediate loss: 32% of breached organizations paid regulatory fines in IBM’s study, and nearly half of those fines exceeded $100,000.

Given that context, security has to be a core architectural pillar, decided alongside feature scope.

Common security threats facing mobile banking apps

Building a secure application requires an explicit, technical understanding of modern attack strategies. Malicious actors continuously target vulnerabilities across mobile binaries, network transit layers, backend database integrations, and more.

- Account takeover happens when attackers gain control of a legitimate user’s account, typically as the end goal of several of the techniques below rather than a standalone method. Once inside, attackers move fast: adding beneficiaries, disabling alerts, and initiating transfers before anyone notices the change.

- Credential stuffing automates login attempts using credentials leaked in unrelated breaches. Even a low success rate yields working accounts at scale when tested against millions of leaked password pairs, and weak bot protection or missing velocity checks make the attack easy to scale further.

- Phishing and smishing impersonate a bank through email, SMS, or messaging apps, redirecting victims to clone login pages. Advanced versions proxy the login in real time: the victim enters a one-time passcode, and the attacker uses it within seconds, before the code expires.

- Banking Trojans and malware infect a device and monitor activity in the background, often disguised as a legitimate app. More advanced variants intercept SMS messages, capture push-based authentication prompts, or abuse accessibility permissions to gain deeper control of the device.

- Overlay attacks display a fake banking interface on top of the real app to capture credentials as the user types them. The overlay is often visually indistinguishable from the genuine login screen.

- Reverse engineering involves decompiling the app to study authentication flows, API endpoints, and business logic. Weak obfuscation makes this dramatically easier for an attacker, and once the flows are exposed, tampered versions of the app can strip out certificate validation entirely.

- API attacks exploit missing authorization checks or predictable identifiers to access data across accounts. A recent survey found that 99% of organizations reported an API security incident within the past 12 months, and more than a third reported sensitive data exposure or a privacy incident as a result.

- Man-in-the-middle (MITM) attacks intercept traffic between app and server, especially on public Wi-Fi, when certificate validation is weak or misconfigured. Flawed pinning logic in edge-case error handling is a common, often overlooked entry point.

- Session hijacking exploits poorly managed session tokens (e.g., long lifetimes, weak rotation, or insecure storage) to replay a valid session without requiring credentials. Tokens leaked through logs or memory inspection on a rooted device create the same exposure.

- SIM swap attacks trick a telecom provider into porting a victim’s number to a new SIM, redirecting SMS-based one-time codes straight to the attacker. The FBI’s IC3 logged nearly $26 million in reported SIM swap losses in a single year, underscoring how costly SMS-only verification can be.

- Rooted or jailbroken devices weaken platform-level sandboxing, giving malware higher privileges and making security checks easier to bypass. Apps that don’t detect this risk end up trusting a device that’s already compromised.

- Third-party SDK vulnerabilities introduce risk through dependencies used for analytics, payments, or biometrics. A single vulnerable library can expose the whole app, and exposure often begins well before the next scheduled dependency scan catches it.

- Business logic abuse exploits process gaps rather than code bugs: rapid transfers timed to beat velocity checks or manipulated beneficiary-approval timing. These scenarios need realistic abuse simulations to catch, since static code scanning won’t surface them.

- Insecure local storage or logging makes tokens, transaction details, or personal data accessible to anyone who extracts data from a compromised device, whether through malware, a backup file, or direct access to the device.

- App cloning and IP theft involve repackaging a legitimate app with malicious code and distributing it via phishing campaigns or unofficial app stores. Users who sideload these clones often hand over credentials without realizing the app isn’t genuine.

Mobile banking security best practices

Building a secure mobile banking app is about combining multiple layers of protection that work together. Every layer should assume another one may eventually fail. This defense-in-depth approach reduces the likelihood that a single vulnerability leads to a full account compromise.

Below are the most important security practices every banking application should implement.

- Multi-factor authentication (MFA) requires users to verify their identity by combining separate validation factors: something they know (a complex password), something they have (a cryptographically bound mobile device), and something they are (verified biometric data).

- Biometrics (fingerprint, facial recognition, or voice) provide strong, low-friction verification for device unlock and re-entry. They work best when paired with a fallback method, since not every user enrolls biometrics and devices occasionally fail to read them.

- Device binding links a session to a specific verified device, so a login attempt from a new device automatically triggers extra scrutiny, such as reauthentication or a temporary hold on high-risk actions.

- End-to-end encryption keeps transaction data unreadable to anyone but the sender and intended recipient throughout its journey, closing off the interception risk that MITM attacks depend on.

- Transport Layer Security (TLS) and Secure Socket Layer (SSL) pinning embed the expected server certificate directly in the app, so it only trusts genuine servers even if a device’s certificate store is compromised.

- Secure API design enforces rate limiting, strict input validation, and least-privilege access on every endpoint, so no single compromised credential can reach more data than that specific function requires.

- Secure session management uses short-lived tokens, strict renewal rules, and immediate invalidation after logout or a risk event, directly closing the gap that session hijacking exploits.

- Secure local storage relies on platform-backed keystores (iOS Keychain, Android Keystore) rather than plaintext files for anything sensitive, including cached tokens and transaction history.

- Code obfuscation makes an app difficult to reverse-engineer, protecting encryption keys and business logic from static analysis tools. It works best as one layer in a broader strategy, not a standalone defense.

- Runtime Application Self-Protection (RASP) detects and blocks tampering, debugging, or code injection while the app is actually running, catching manipulation that static scanning alone would miss.

- Root and jailbreak detection flags compromised devices so the app can restrict functionality or require step-up authentication, rather than trusting a device whose sandboxing has already been weakened.

- Malware detection monitors known overlay and accessibility-abuse patterns rather than assuming the device is clean, since a growing share of fraud now originates from compromised devices rather than from the app itself.

- Runtime integrity checks verify that the app hasn’t been modified since it was signed and shipped, typically by running checks at random points during execution.

- Certificate pinning works alongside TLS to close the specific gap that attackers exploit in compromised certificate stores, though fallback handling needs careful design to ensure a certificate rotation doesn’t accidentally lock out legitimate users.

- Tokenization replaces sensitive identifiers with meaningless tokens that carry no value outside the system, limiting the damage if a token is ever exposed.

- Threat monitoring gives security teams real-time visibility into which users, devices, and app versions are associated with active attacks, so engineering can build targeted protections into the next release rather than reacting after the fact.

- AI-driven fraud detection analyzes transaction patterns for anomalies in real time, flagging or blocking high-risk transactions before funds move.

- Behavioral biometrics learn typing rhythm, swipe pressure, and device-holding angle, catching account takeover even after credentials are compromised, since the behavioral signature is much harder for an attacker to replicate than a password.

Even a solid stack of these controls has known limits worth planning around. Attackers use deepfake technology and device spoofing to get past Know Your Customer (KYC) checks. Trojan malware intercepts MFA codes directly off the device before the user notices. Moreover, attackers have found ways to manipulate the communication between secure SDKs and the apps that embed them. None of this means these controls aren’t worth building — it means no single layer should be treated as sufficient on its own.

Tip: start with MFA, biometrics, TLS 1.3, certificate pinning, secure session management, and basic fraud detection. Then layer in RASP, attestation, behavioral biometrics, and advanced threat monitoring as risk and budget allow.

Regulatory compliance requirements

Security controls are only one part of building a trustworthy mobile banking application. Companies must also demonstrate that their systems meet strict regulatory and industry requirements designed to protect customer data, prevent fraud, and maintain operational resilience.

The specific regulations that apply depend on several factors, including:

- Geography (where you operate and where your users are)

- Business model (retail bank, neobank, credit union, fintech, payment processor, etc.)

- Data sensitivity (types of data processed, such as PII, PAN, credentials, etc.)

While requirements vary across regions and industries, most frameworks focus on the same core security principles:

- Protecting customer data through encryption and access controls

- Maintaining application and code integrity

- Securing the mobile environment through device and runtime protections

- Protecting APIs and communication channels

- Implementing strong authentication and authorization

- Maintaining audit trails and monitoring capabilities

- Continuously testing and improving security controls

Below are the most important compliance frameworks organizations should consider when developing mobile banking applications.

| Framework | What it covers | Applies to |

|---|---|---|

| PCI DSS | Payment card data security | Any app processing card transactions |

| PSD2 | Strong Customer Authentication (SCA), Open Banking APIs | Banks and fintechs operating in the EU/UK |

| GDPR | Data privacy, consent, right to erasure | Any app serving EU users |

| GLBA | Financial data safeguards, written security program | U.S. financial institutions |

| FFIEC | Supervisory expectations for layered security | U.S. banks and credit unions |

| ISO 27001 | Information security management system | Enterprise banking and fintech platforms |

| SOC 2 | Security, availability, and confidentiality audit | Cloud and technology vendors serving banks |

| OWASP MASVS & MSTG | Mobile-specific technical security benchmarks | Development and security testing teams |

| Regional (MAS TRM, RBI, NIST) | Local technology risk and data-residency rules | Institutions operating in that jurisdiction |

Mobile banking app development process

While exact timelines vary depending on complexity, regulatory requirements, and integration needs, most mobile banking projects follow a structured development lifecycle.

1. Discovery and planning

- Define user personas and core journeys.

- Identify target markets, payment rails, and licensing requirements.

- Scope MVP with compliance as a first-class constraint.

- Produce a technical discovery document covering integrations, data flows, and the security model.

2. Compliance analysis

- Map jurisdictions, business model, and data types.

- Translate PCI DSS, PSD2, GDPR, GLBA, etc., into concrete security requirements.

- Define abuse cases (ATO, fraud transfers, social engineering) and compliance evidence needs.

3. UX/UI design

Design for confidence and control:

- Clear confirmation before transactions.

- Obvious error states with recovery paths.

- Accessibility (WCAG 2.1 AA as baseline).

- Usability testing with real users.

Balance security and UX by applying stronger controls where risk is high and removing friction where it is not. Use risk-based authentication, biometrics, and predictable step-up flows, and measure success with auth success rates, step-up abandonment, and fraud loss metrics.

4. Architecture

- Define data isolation, authentication flow, API gateway design, and encryption approach.

- Create system architecture diagrams, data flow maps, and threat models.

- Plan infrastructure provisioning and integration points with core banking or BaaS.

5. Backend development

- Build APIs with strong authentication, strict authorization, and rate limiting.

- Implement secure session and token management.

- Integrate with core banking systems, payment rails, and third-party services.

6. Mobile development

- Implement authentication, session management, and device binding first.

- Build account data APIs, transaction history, transfers, card management, and payments.

- Apply mobile-specific hardening (obfuscation, integrity checks, root detection).

7. API development

- Use OAuth 2.0 + Proof Key for Code Exchange (PKCE) and OpenID Connect (OIDC).

- Apply object-level authorization, input validation, and safe error handling.

- Monitor usage patterns and enforce rate limits.

8. Security implementation

- Embed encryption, certificate pinning, and secure storage from the start.

- Integrate RASP, attestation, and behavioral biometrics as needed.

- Align with OWASP MASVS and regional regulations.

9. Testing

- Perform Static application security testing (SAST), Dynamic application security testing (DAST), dependency scanning, and secret detection in CI.

- Conduct penetration testing by qualified third parties.

- Run abuse-resistant tests: fuzzing, negative testing, transaction abuse scenarios.

10. Deployment

- Use staged rollouts (beta → 5% → 25% → 100%).

- Enable debug-free, hardened release builds.

- Enforce branch protections and signed builds where feasible.

11. Monitoring

- Track real-time errors, transaction success rates, and API latency.

- Monitor security events and fraud signals.

- Maintain immutable, correlated audit logs with proper retention.

Secure software development lifecycle

Beyond the phase-by-phase process above, a mature secure SDLC (Software Development Lifecycle) needs a few structural elements running underneath it:

- Security ownership and operating model. Establish a comprehensive Responsibility Assignment Matrix (RACI) that links Product, Engineering, DevOps, and Security compliance teams together. Define explicit key performance indicators (KPIs) to track vulnerability remediation timelines.

- Security requirements and risk baseline. Translate complex legal mandates into clear non-functional software requirements, ensuring that explicit data classification standards are enforced across all development environments.

- Threat modeling for banking journeys. Analyze target user journeys to systematically map technical boundaries and build automated test cases to protect against known abuse patterns.

- Secure architecture and data flows. Enforce strict service isolation across all internal microservices networks, leverage short-lived JSON Web Tokens, and apply the principle of least privilege across all database connections.

- Identity, access, and customer authentication. Build secure, adaptive authentication engines on the server side and ensure that account recovery pathways receive the same security controls as core login windows.

- Secure coding standards for mobile and backend. Enforce comprehensive input sanitization routines, block verbose error-generation paths in production builds, and mandate thorough code reviews aligned with OWASP MASVS guidelines.

- Secrets and crypto handling. Eliminate hardcoded variables by leveraging enterprise cloud key management services. Store all production tokens inside isolated hardware security modules with strict access controls.

- Third-party and supply chain security. Maintain an automated Software Bill of Materials (SBOM) to track all application dependencies.

- CI/CD security automation and gates. Embed automated SAST, dependency analysis, and secret-detection scanners directly into code validation loops, establishing automated release gates that block any build containing high-severity findings.

- Mobile-specific hardening and testing. Hardcode multi-layered reverse-engineering protections, apply polymorphic binary obfuscation, and run extensive integrity-bypass simulations before shipping software to application storefronts.

- API and abuse-resistant testing. Run automated fuzzing cycles across all external API endpoints and execute functional transaction-abuse simulations to ensure codebases handle payment conditions safely.

- Release security reviews and sign-off. Enforce mandatory pre-release security validation checks and secure formal executive sign-off before allowing any financial technology build to hit production servers.

- Monitoring, fraud signals, and audit trails. Build immutable, cryptographically signed logging trails to record security events, ensuring that telemetry feeds instantly into automated anti-fraud analytics engines.

- Incident response and post-release maintenance. Prepare detailed operational playbooks to guide teams through zero-day vulnerabilities and credential-stuffing attacks, and establish clear patch-delivery service-level agreements (SLAs) to ship critical updates quickly.

Balancing security and UX in design

Good banking UX has one job: make users feel confident and in control of their money. Strong controls and good UX aren’t actually in conflict — they work together when teams apply friction deliberately rather than uniformly.

Authentication should adapt to risk rather than following static rules. Checking a balance should feel instant; adding a new beneficiary or moving a large sum should trigger step-up verification. Biometrics work well for device unlock and quick re-entry, but high-risk transactions still deserve an additional factor or explicit confirmation. Session timeouts should scale with what’s at stake — longer for viewing history, shorter for wire transfers — and background token refresh avoids logging people out unnecessarily.

Users tolerate friction they understand. Triggering step-up authentication transparently, for a genuinely new device or an unusually large transfer, builds trust. Random, inconsistent prompts erode it. The same logic applies to onboarding: progressive data collection during eKYC (electronic Know Your Customer) beats a long upfront form and reduces abandonment without cutting corners on verification. Passwordless approaches like passkeys reduce password fatigue and, by extension, the risk of credential stuffing.

Common mistakes to avoid

These patterns recur in banking app projects that stall, blow the budget, or ship with critical gaps.

- Hardcoding secrets or API keys directly in the client, where anyone who decompiles the app can find them.

- Shipping APIs without rate limiting or proper authorization checks leaves the door open to the exact abuse patterns covered earlier.

- Storing sensitive data locally without encryption turns a lost or stolen device into a data breach.

- Relying on SMS one-time passwords as the only second factor, despite how easily SIM swap attacks defeat them.

- Managing sessions poorly (e.g., long lifetimes, weak rotation, pr no forced logout on risk events) widens the window for session hijacking.

- Skipping penetration testing until just before launch, leaving no time to fix what it finds.

- Treating accessibility as a post-launch fix rather than a design requirement, even though WCAG 2.1 AA compliance is a legal expectation in many markets.

- Delaying compliance review until development is largely complete, which is how teams end up rebuilding authentication flows weeks before launch.

- Trusting client-side validation as a security boundary, when the mobile client should never be treated as a trusted enforcement point.

- Integrating third-party SDKs without vetting their permissions or vulnerability history, since a single compromised dependency can expose the entire app.

- Neglecting offline and low-connectivity scenarios — banking applications must account for situations where users have unreliable network access.

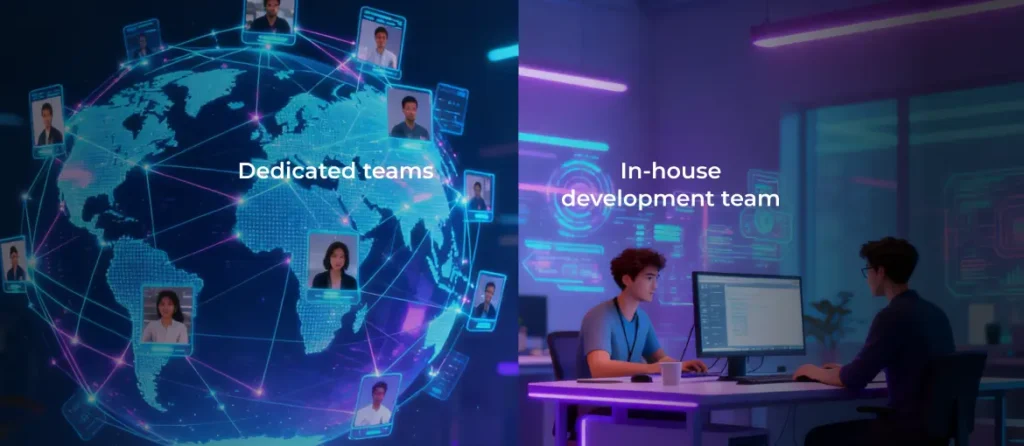

Build vs. partner: choosing the right development approach

Choosing how to build a mobile banking application depends on factors such as regulatory obligations, internal engineering capabilities, desired level of customization, time-to-market goals, and long-term ownership requirements. There are three common paths: building entirely in-house, using a Banking-as-a-Service (BaaS) or white-label platform, and partnering with an experienced development team to build a custom solution. Each approach has advantages and trade-offs.

Building in-house: maximum control, maximum responsibility

Building a banking app entirely with an internal team provides the highest level of control over architecture decisions, security practices, product roadmap, customer experience, and infrastructure ownership. This approach can make sense for large financial institutions with established engineering organizations, dedicated security teams, and experience managing regulated software environments.

However, building internally also requires significant investment. Organizations need expertise across multiple areas, including mobile engineering, backend development, cloud infrastructure, cybersecurity, compliance, fraud prevention, payment integrations, quality assurance, and regulatory reporting.

Security requirements continue to evolve, and internal teams must continually invest in vulnerability management, penetration testing, secure development practices, threat monitoring, and more. For organizations without existing banking technology expertise, building everything internally can significantly extend timelines and increase operational complexity.

Using BaaS or white-label platforms: faster launch, less customization

Banking-as-a-Service (BaaS) providers and white-label banking platforms allow companies to launch financial products without building every banking capability from scratch. These solutions typically provide access to account infrastructure, payment processing, card issuing capabilities, compliance support, identity verification services, and transaction-processing APIs.

The main advantage is speed. A fintech startup or a smaller financial institution can validate a product idea more quickly without developing an entire banking ecosystem internally. However, this convenience comes with potential limitations, including reduced architectural control, reliance on vendor security practices, limited customization options, platform migration challenges, and recurring licensing costs.

Security responsibilities also need to be clearly defined. Even when a provider handles certain infrastructure components, the organization remains responsible for protecting customer data, securing integrations, and managing application-level risks. A BaaS provider can reduce development effort, but it does not eliminate the need for strong mobile banking security practices.

Collaborating with a technology partner: expertise without building everything internally

For many banks, credit unions, and fintech companies, partnering with an experienced software development team offers a balance between control, speed, and expertise. A development partner can extend internal capabilities without requiring organizations to hire every role permanently. This is especially valuable when internal teams have strong product knowledge but lack specialized expertise in banking application security.

For companies evaluating external partners, it is important to consider factors such as security maturity, financial industry experience, development methodology, communication processes, and long-term support capabilities. A structured evaluation process can help identify a partner that aligns with both technical and business goals.

Where outsourcing and nearshore partnerships fit in banking security

Outsourcing is sometimes viewed as a way to reduce development costs, but for banking applications, the bigger advantage is often access to specialized expertise. A strong nearshore partner can support security-critical areas such as secure architecture reviews, threat modeling, application security testing, API security, cloud security, compliance preparation, and secure CI/CD implementation.

Nearshore partnerships can be particularly effective because they often provide closer time zone alignment, easier collaboration with internal teams, access to broader engineering talent pools, and faster scaling of specialized resources. However, security should be a key selection criterion. Before partnering, companies should evaluate:

- Security certifications and processes

- Experience with regulated industries

- Secure coding practices

- Access control policies

- Vulnerability management procedures

- Incident response processes

What drives cost in secure banking app development

Investments are directly tied to the integration landscape, regulatory scope, and security assurance criteria of your chosen architecture. The table below maps out the primary cost vectors encountered during enterprise development projects:

| Critical cost driver | Technical engineering complexity | Operational impact on project budget |

|---|---|---|

| Regulatory architecture | Cross-border compliance mapping, regional data localization hosting setups, and multi-factor transaction signing | Multiplies baseline architecture timelines and demands expert legal alignment |

| Core banking integration | Interfacing modern mobile code bases with rigid, legacy core banking system APIs and on-premise transactional databases | Consumes significant development resources; legacy documentation often requires extensive custom middleware |

| Security certification | Mandatory external penetration testing sweeps, formal SOC 2 Type II audit tracking, and automated compliance engine setups | Requires dedicated security allocations, external auditor fees, and strict validation testing loops |

| Payment rail connections | Programmatic integration with regional settlement networks, including SWIFT, SEPA, ACH, or real-time payment hubs | Demands rigorous validation testing across disparate networks and strict security standard compliance |

Project scopes dictate development investment ranges. For example, a fintech MVP focused on core transaction rails and secure authentication can be deployed within four to six months. Comprehensive retail applications for community banks require eight to twelve months of development, while enterprise multi-region banking frameworks routinely demand eighteen to twenty-four months.

Case studies: security and compliance in action

A purchase-intelligence and card-linked rewards platform needed to embed cashback and rewards functionality directly inside major banks’ native mobile apps, scaling to more than 170 million monthly active users. AgileEngine built a mobile SDK from scratch, enabling financial institutions to deploy functionality without building it themselves. The engineering team also built scalable, secure streaming data pipelines — using AWS, Lambda, API Gateway, S3, SQS, Kafka, and Apache Spark — to process high-volume transaction data under strict financial industry standards. The result: onboarding time for new bank partners dropped from weeks to hours.

A digital card management platform allows cardholders to manage cards and spending controls directly, helping banks and payment processors cut operational costs. AgileEngine’s nearshore team built proof-of-concept and MVP solutions across web, mobile, and wearable devices, then layered in multi-authentication support, a distributed login system, and secure environment configuration, moving secrets entirely out of the build. The infrastructure work extended to aligning the DevOps pipeline with Dockerization and Kubernetes best practices, protecting cardholder data at every layer.

2026 trends and what’s coming next in banking app security

Passkeys and passwordless login are becoming standard across major banking apps, cutting reliance on the credentials that fuel stuffing attacks in the first place. Because passkeys are bound to a specific device and can’t be phished the way a password can, they close off two of the most common attack paths covered earlier at once.

Adaptive authentication and behavioral biometrics are shifting security decisions from static rules to continuous, context-aware risk scoring. Instead of a fixed MFA prompt at every login, systems increasingly weigh device history, location, and behavioral patterns together, reserving friction for the moments that actually warrant it.

AI-driven fraud detection is moving from rule-based flagging toward models that catch novel fraud patterns in real time, not just known ones. This matters most for business logic abuse and coordinated fraud rings, where static rules tend to miss the pattern until after the damage is done.

As quantum computing technology advances, standard encryption models like RSA and ECC will eventually face severe decryption risks. Forward-thinking software architects are beginning to test post-quantum cryptography (PQC) algorithms within their secure data pipelines, ensuring long-term data protection against next-generation computing threats.

Generative Artificial Intelligence (GenAI) is transforming front-office operations by powering intelligent customer service interfaces, managing tier-one customer service triage, and parsing complex investment documentation. However, due to data security concerns, strict boundaries are imposed on these models. Engineering teams deploy GenAI within sandboxed environments, stripping all customer PII and using strict tokenization frameworks to prevent data leakage into base training sets.

Conclusion

Developing a successful modern fintech platform requires a comprehensive strategy that treats security and compliance as fundamental design requirements. Technical leaders must implement multi-layered defenses that shield compiled binaries, secure data-transmission tunnels, and harden high-volume backend streaming pipelines. Ultimately, the market favors platforms that elegantly balance bulletproof asset protection with an intuitive, seamless user experience.

Implementing resilient financial software solutions requires careful structural planning, proper engineering team expertise, and a strategic approach to system integration. Professional software outsourcing services ensure your project meets strict compliance mandates while staying within budget and timeline parameters.

Ready to scale your engineering capability and upgrade your financial platform’s defense?

Boost development efficiency without breaking the budget. Our dedicated teams offer 2X cost savings, delivering in-house-level quality

Let’s chatFAQ

Mobile banking applications are among the most heavily shielded pieces of commercial software in the technology sector, utilizing advanced multi-layered defenses. They combine hardware-backed biometric verification and AES-256 data encryption with real-time client-side RASP defenses that actively block code tampering and screen scraping. When engineered using strict Zero Trust guidelines, they isolate transaction processing from common endpoint vulnerabilities.

A focused MVP with core payments and authentication typically takes a few months to build. A full-featured app with core banking system integration and multiple compliance certifications usually takes closer to a year, and multi-region enterprise platforms can run well beyond that.

Frontend engineering relies on native Swift (iOS) and Kotlin (Android) for absolute control over hardware enclaves, or cross-platform frameworks like Flutter and React Native for unified deployment. Backend ecosystems handle transaction processing using Java Spring Boot, Node.js, and PostgreSQL database clusters. Real-time anti-fraud pipelines leverage distributed event platforms like Apache Kafka paired with high-velocity Apache Spark analytical computing engines.

Yes. Most fintechs either partner with a licensed bank as a sponsor or use a Banking-as-a-Service provider that already holds the necessary licenses and regulatory relationships.

At minimum, before every major release, plus periodic testing on a regular cadence (commonly quarterly or semi-annually) to catch issues introduced by new features or shifting infrastructure.

![A smartphone and a tablet with monetization elements (banner ad and in-app purchase button) displayed on the screen]](https://agileengine.com/wp-content/uploads/2026/03/How-Do-Free-Apps-Make-Money_-Monetization-Explained.webp)